Short Covering or a Relief Rally

April 6, 2026

Market Roundup & The Week in Review

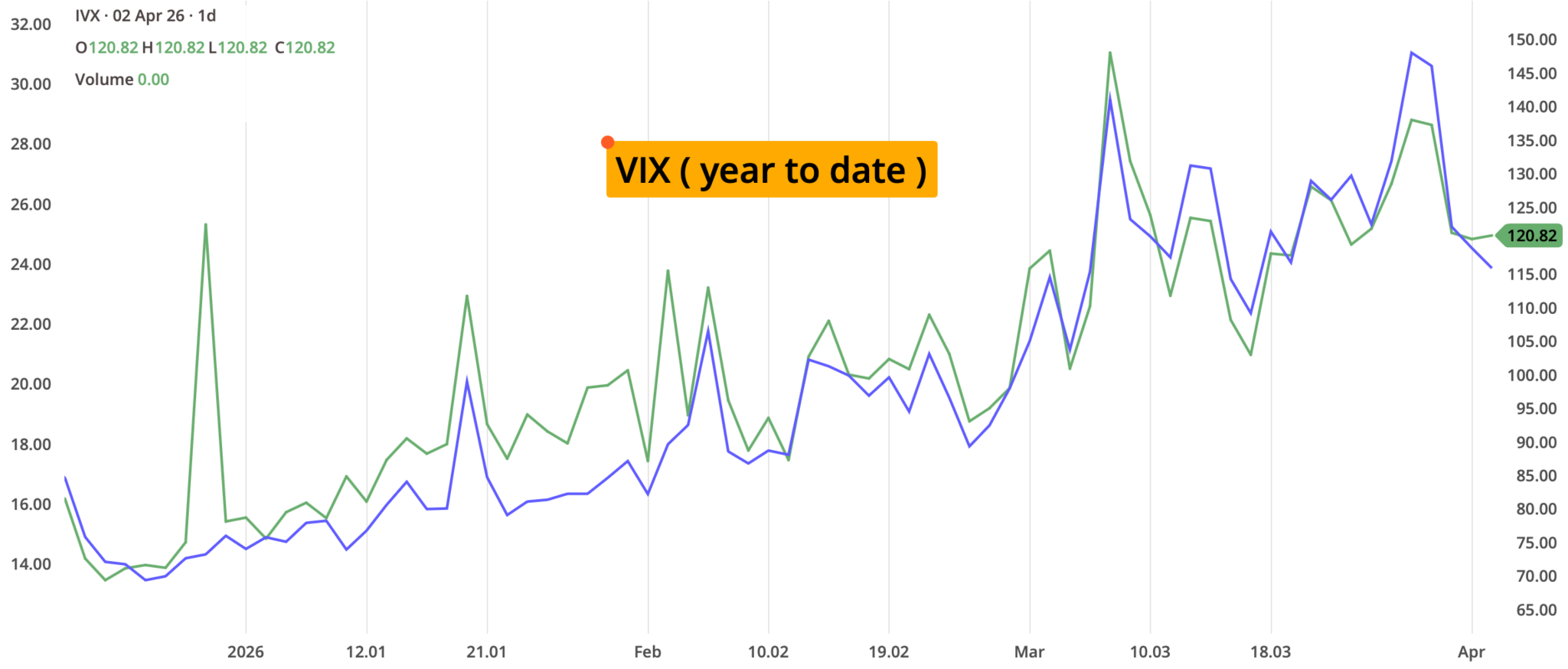

The final week of March and the transition into April could probably be described as a "Volatility Vacuum." After weeks of geopolitical posturing and a 10-year yield that seemed intent on breaking 4.50%, the market staged a massive relief rally that saw the VIX collapse over 23% in just four sessions. This "risk-on" flood wasn't necessarily sparked by a change in fundamentals, but rather by the absence of a "worst-case scenario" manifesting in the Middle East.

However, the "Goldilocks" narrative remains under pressure. While the ISM Manufacturing data finally showed signs of life, it also brought a reminder that input prices are rising. The "low-hire, low-fire" labor trend might be shifting; Friday's massive "beat" in the Unemployment report could be a double-edged sword. While it proves the consumer is employed, it probably gives the Fed all the cover it needs to keep rates "higher for longer," potentially pushing any hope of a June cut off the table.

As the month of April starts, the focus will likely shift from macro headlines to micro fundamentals. With the "Big Banks" reporting on April 10th, the market is looking for confirmation that the "wealth effect" is still driving consumer spending despite $4.00+ gasoline. Investors could see a period of consolidation here as the indices catch their breath, especially as the Q1 earnings "whisper numbers" begin to leak.

Basically last week was defined by a massive collapse in volatility, a resurgent labor market, and a shift from macro fears to earnings anticipation. Will focus start to shift away from oil and towards fundamentals.

As the second quarter of 2026 begins, the divergence between "price action" and "fundamental reality" is becoming impossible to ignore. Last week's massive relief rally and the subsequent collapse of the VIX suggest a market that is desperate to look past geopolitical strife. However, the "Secular Strains" are beginning to show in the data.

With a "blowout" jobs report of 178,000 released while the exchanges were dark on Friday, will a strong labor market spell "good news" for stocks, or will it simply be the fuel that keeps the Fed's hawkish fire burning?

Was last week a genuine bottom or simply a "Volatility Vacuum" that will be filled the moment the first big bank misses an earnings target on April 10th. The market tone appears to be "fragile" - was that short covering or risk on?

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

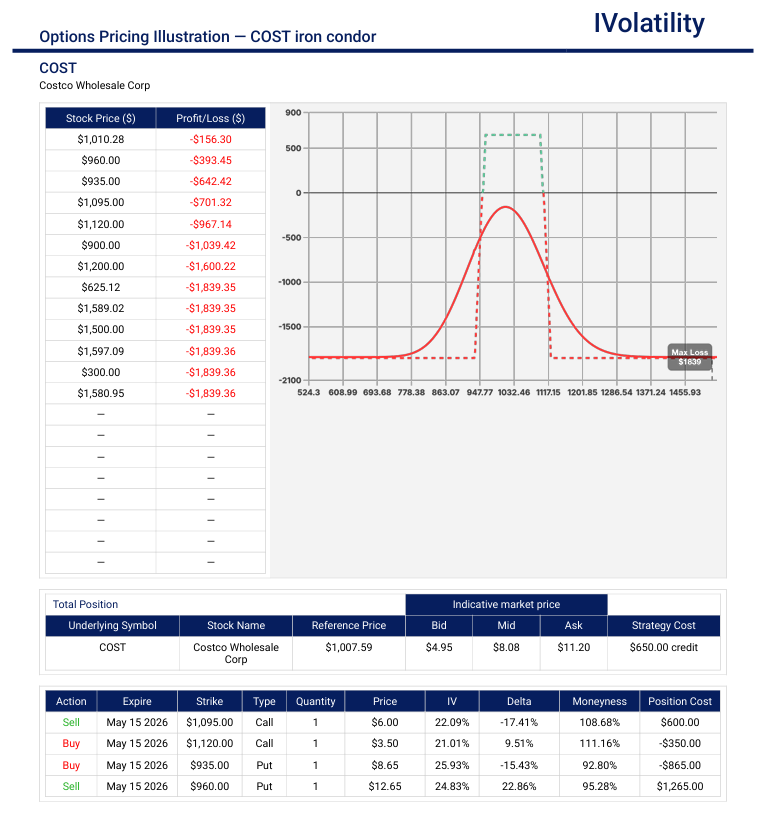

- COST (closed at 1040.80 on Friday, Apr 3rd)

COST has shown strong resilience, recovering from a March dip near $965. It successfully reclaimed its 50-day moving average and is currently trading just above the psychologically important $1,000 level. - Strategy: Sell a May iron condor

- Setup: Sell the may 935/960 put spread along with the 1095/1120 call spread

- Credit: $650

- Breakevens: around 956 and 1100

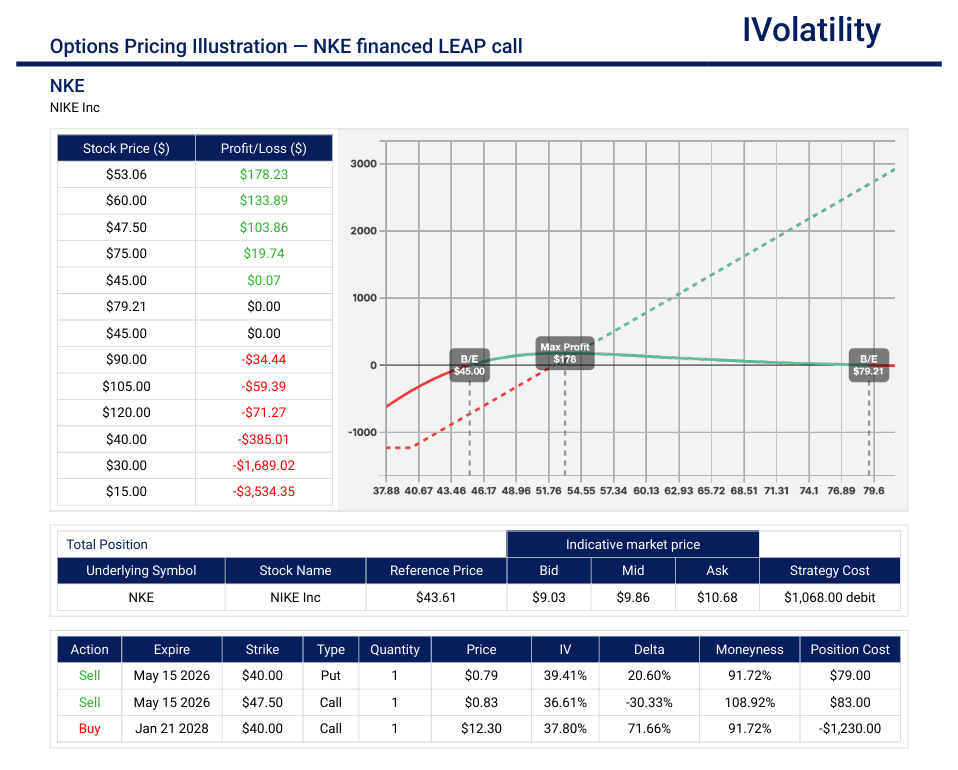

- NKE (closed at 44.18 on Friday, Apr 3rd)

After a significant pullback from its 2021 highs, Nike is trading at a more reasonable P/E multiple than it has in years. For a "forever" hold, an investor may have a chance to buy a premium global leader without paying the "hype premium" of $170+. - Strategy: Financed LEAP call

- Set up: Buy the Jan2028 40call / sell the May2026 40/47.5 strangle

- Debit paid: $1070

Movement of the Major Market Indices:

The week from March 30th through April 3rd was characterized by a significant relief rally following the volatility of late March. The major averages saw strong gains and the VIX retraced nearly 25% from its recent highs. Could this be a signal of a notable shift in market sentiment?

| INDEX | UP | DOWN |

| SPY | 3.43% | |

| QQQ | 3.64% | |

| IWM | 3.41% | |

| DIA | 2.89% | |

| GLD | -1.92% | |

| BTC/USD | 0.50% | |

| TLT | -2.93% | |

| Crude Oil | 9.64% | |

| VIX | -23.12% |

Movement of the Major Market Sectors:

The week saw a strong broad-based recovery, with Technology and Financials leading the charge as geopolitical tensions showed signs of stabilizing mid-week.

| SECTOR | UP | DOWN |

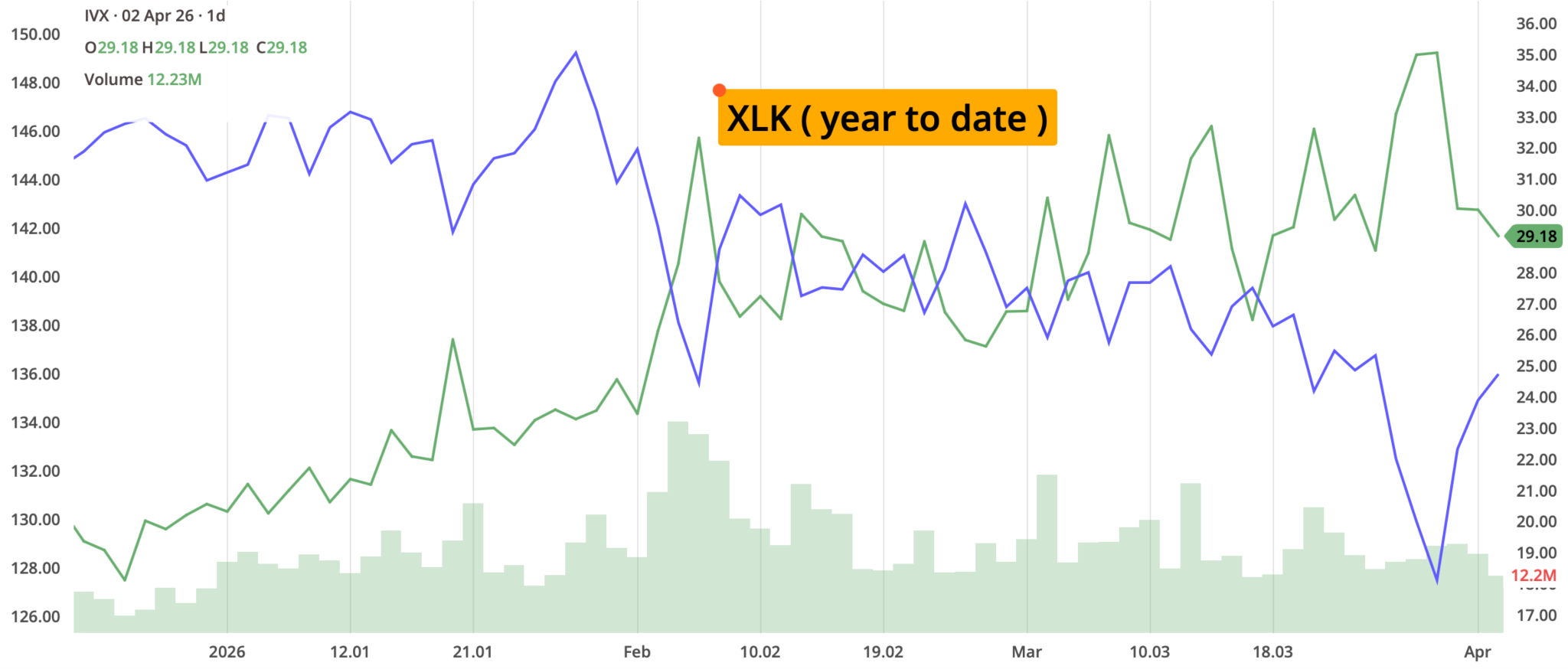

| TECH (XLK) | 3.88% | |

| FINANCIALS (XL) | 3.52% | |

| INDUSTRIALS (XLI) | 3.14% | |

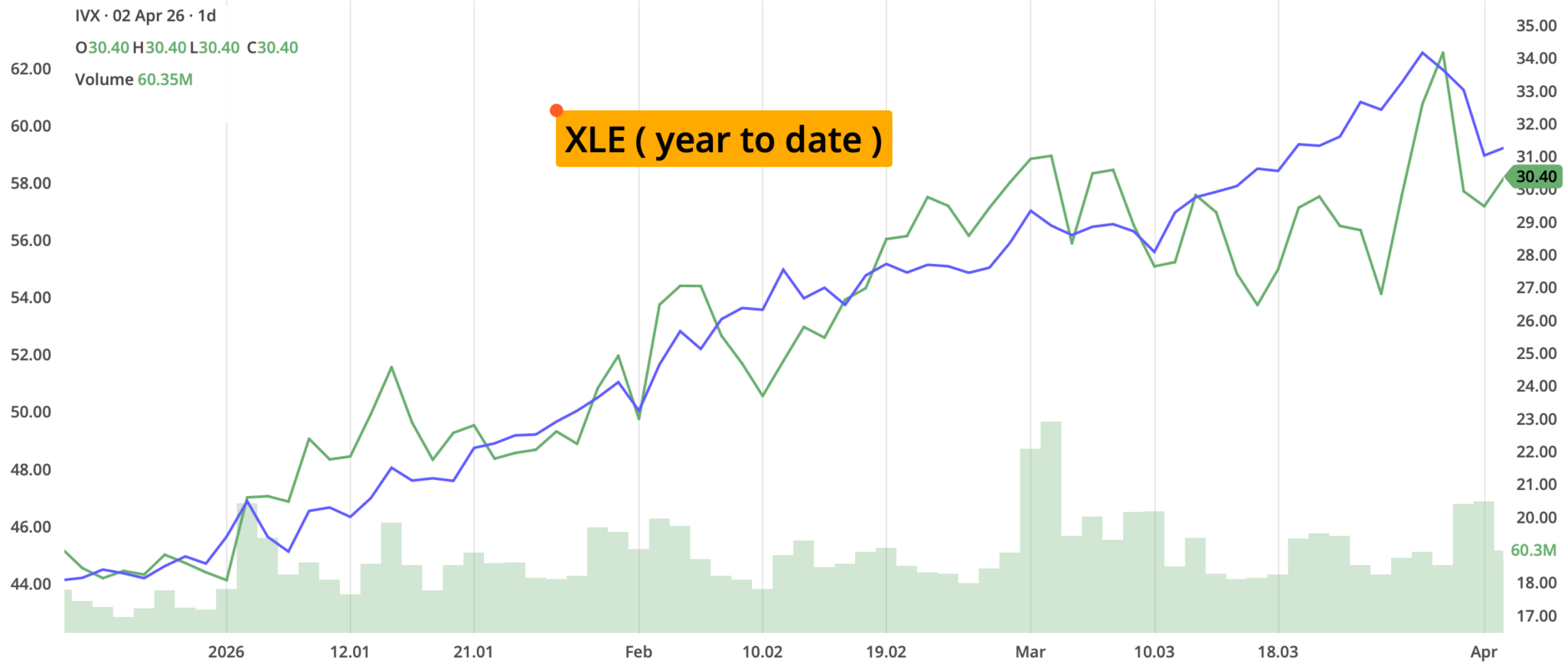

| ENERGY XLE | -5.29% | |

| HEALTHCARE (XLV) | 2.45% | |

| UTILITIES (XLU) | 1.98% | |

| MATERIALS (XLB) | 2.12% | |

| REAL ESTATE (XLRE) | 2.65% | |

| CONSUMER STAPLES (XLP) | 0.13% | |

| CONSUMER DISCRETIONARY (XLY) | -2.34% |

- XLK (Technology): Led the market recovery as investors seemed to return to AI infrastructure plays and mega-cap growth following the stabilization of the 10-year yield.

- XLF (Financials): Benefited from a steepening yield curve and anticipation of strong net interest income commentary from financials releasing earnings starting April 10th.

- XLI (Industrials): Boosted by signs of manufacturing expansion in the ISM PMI data and continued capital expenditure in the aerospace and defense industries.

- XLE (Energy): Pulled back sharply as initial fears of a total supply shutdown in the Middle East seemed to ease, leading to a "sell the news" event in crude-heavy names.

- XLV (Health Care): Saw a modest rebound as capital appeared to rotate into managed care and biotech after an oversold period in late March.

- XLU (Utilities): Gained ground as a "defensive growth" play, with investors increasingly viewing utilities as essential beneficiaries of AI-driven data center power demand.

- XLB (Materials): Performance was driven by a rebound in base metals and construction materials as domestic infrastructure projects appeared to continue to move forward.

- XLRE (Real Estate): Recovered from recent lows as the pause in the 10-year yield's ascent provided some relief for commercial REITs and residential developers.

- XLP (Consumer Staples): Largely flat for the week as investors appeared to rotate away from defensive "safe havens" in favor of more aggressive growth sectors like Tech and Financials.

- XLY (Consumer Discretionary): Supported by resilient consumer spending data and a rally in major retail and automotive components.

Notable gainers for the week of March 30th–Apr 3rd:

As the 10-year yield stabilized mid-week, capital aggressively rotated back into "Tier 1" technology and cybersecurity. Investors moved away from speculative names and toward companies with proven free cash flow and a direct "toll booth" position in the AI infrastructure build-out.

- ServiceNow (NOW) rallied 5.59% as enterprise software caught a bid following a successful AI summit where they demonstrated new generative workflows.

- Palo Alto Networks (PANW) popped 4.99%. Cybersecurity remains a high-conviction area and PANW benefited from broader sector rotation back into "Mission Critical" tech infrastructure.

- Cboe Global Markets (CBOE) rose 3.41% despite the VIX drop, the high-volume environment of late March continues to support their exchange revenue outlook.

Notable losers for the week of Mar 30th–Apr 3rd:

The primary downward pressure last week came from a "double-headed monster" of rising input costs (oil/energy) and evidence that the American consumer is finally starting to push back against higher prices. This led to a sharp de-risking in logistics and semiconductor cyclicality.

- Sysco Corporation (SYY) plummeted over 15%after providing a cautious outlook on restaurant volume, suggesting that higher energy costs may finally crimping diner frequency.

- Micron Technology (MU) dropped nearly 10% after facing heavy profit-taking and a downgrade related to "circular financing" concerns within the broader semiconductor industry.

- Western Digital (WDC) shed over 8.5% perhaps in sympathy with Micron. Investors are showing jitters about the sustainability of the current storage pricing cycle.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

Markets opened with a flash of optimism on ceasefire rumors, but the mood soured instantly as U.S. oil topped $100 per barrel. The S&P 500 erased early gains to finish in the red. Uncertainty regarding the Strait of Hormuz remained the primary weight on sentiment, with the Russell 2000 (IWM) leading the decline (-1.5%) as small caps felt the pinch of rising input costs.

Tuesday's Markets and News:

The final day of Q1 saw a massive trend reversal. Reports of progress in U.S.-Iran negotiations sent oil prices lower and sparked a powerful rally. The Nasdaq Composite surged nearly 4%, its best day in nearly a year, as investors aggressively bought the dip in oversold AI and semiconductor names. Despite the bounce, many indices ended the quarter roughly 5%–9% below their all-time highs.

Wednesday's Markets and News:

The "April Fools" session held onto its gains as President Trump suggested Iran had requested a ceasefire. The S&P 500 rose another 0.6%, buoyed by better-than-expected retail sales and a manufacturing PMI that hinted at domestic resilience. Big Tech names like Alphabet and Nvidia provided the heavy lifting, while defensive sectors like Utilities and Energy took a breather.

Thursday's Markets and News:

The morning saw a sharp "risk-off" move after fresh rhetoric from the White House suggested a de-escalation was not yet imminent. The Dow fell over 500 points in early trading as Brent crude spiked back toward $110. However, the market staged a late-day "Volatility Vacuum" recovery, with the VIX collapsing over 20% by the close as traders positioned for the long weekend, betting that the "worst-case" was already priced in.

Friday's Markets and News:

While U.S. exchanges were closed for Good Friday, the Bureau of Labor Statistics released the Unemployment report. March Non-Farm Payrolls blew out expectations at +178,000 (vs. 60,000 expected), essentially erasing the weakness of the prior month. Equity futures and bonds sold off in the abbreviated session, as the data probably removes any lingering hope for a Fed rate cut in the first half of 2026.

Notable Earnings (Apr 6th–Apr 10th)

Investors will be in that "calm before the storm" period just before the major banks kick off the Q1 earnings season. There are a few key names that could serve as important indicators for AI infrastructure and consumer health.

The actual date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday: no notable earnings announcements schedulede

Tuesday: AEHR / GBX / LEVI / SKIL

Wednesday: APLD / DAL / STZ

Thursday: WDFC / WLTH

Friday: BLK

According to earningswhisper.com, the expectations are :

Beat: AEHR / DAL / STZ / LEVI / GBX / SKIL

Miss: APLD

Economic Calendar (Apr 6th–Apr 10th)

The daily schedule of notable economic data releases is:

Monday, Apr 6th

- ISM Services PMI

This report is a vital health check on the services sector, which drives roughly 80% of US GDP. Investors should be able to determine whether high input costs are finally starting to cool expansion. - POTUS deadline for Iran at 5pmEST

Tuesday, Apr 7th

- Quiet day; no major US economic data release is planned

Wednesday, Apr 8th

- FOMC Minutes of March meeting

Traders will probably examine these notes for any "hawkish" or "dovish" nuances regarding the committee's internal debate over the 2026 rate path and balance sheet reduction.

Thursday, Apr 9th

- Initial Jobless Claims

This weekly gauge will be watched closely to see if the "low-hire, low-fire" trend continues or if layoffs are starting to creep up in the tech and industrial sectors. - PCE (personal income and outlays)

As the Fed's preferred inflation metric, this data could confirm whether inflation is truly trending toward the 2% target or remains stubbornly "sticky".

Friday, Apr 10th

- CPI

This is the high-stakes print of the week; a "hot" reading could spark a sharp rotation out of growth stocks and into more defensive sectors. - University of Michigan Consumer Sentiment (preliminary)

This provides an early look at how inflation expectations are affecting the American consumer’s willingness to spend. This preliminary reading often tends to move the market more than subsequent revisions.

Something to think about...

The Rise of the "Ghost in the Machine": Agentic AI

We've long been used to algorithmic trading—the "black boxes" that execute based on pre-set math. But as we move further into 2026, we are witnessing the birth of Agentic AI in the markets. Unlike traditional algos, these are autonomous AI agents capable of "reasoning." They don't just execute a trade; they monitor the news, listen to Fed speeches in real-time, scan social sentiment, and then decide which strategy to deploy—backtesting and stress-testing it in seconds before a human even sees the headline.

The question now is what happens to market structure when 70% or more of the volume is driven by machines that are simulating outcomes against each other? We might be entering an era where price action is less a reflection of human economic fundamentals and more a "recursive artifact" of AI agents playing a high-speed game of chess.

When the VIX collapses 23% in four days, is it because humans feel safer, or because the agents have all calculated that the "volatility trade" is officially crowded? In such an environment, traders may not be just competing against "the market" anymore—they are competing against a hive mind that never sleeps and processes a million tokens of context while you're still pouring your first cup of coffee.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.